HRAs and HSAs can be Compatible

December 2, 2022

Employers offering a high deductible health plan (HDHP) may want to offer HDHP participants a health reimbursement arrangement (HRA) to buy down the deductible. The HRA design will determine whether HDHP participants can also maintain eligibility to contribute to a health savings account (HSA).

An HRA must be funded by employer dollars and never by employee contributions. An HRA offered alongside, or integrated with, an HDHP will generally be structured in one of three ways:

- General-purpose HRA: Immediately available to reimburse qualifying medical expenses up to a certain annual dollar limit.

- Post-deductible HRA: Not available until after a participant incurs claims up to a set dollar amount, and thereafter available to reimburse qualifying medical expenses up to a certain annual dollar limit.

- Limited-purpose HRA: Immediately available, but only for limited-scope dental and vision expenses up to a certain annual dollar limit.

A general-purpose HRA offering will make all participants ineligible to contribute to an HSA. Having access to reimbursement for qualifying medical expenses prior to incurring claims of at least $1,500 for single HDHP coverage, or $3,000 for family HDHP coverage, in 2023 is disqualifying coverage for purposes of HSA-eligibility. This is true regardless of whether the participants receive any reimbursement from the HRA.

However, a post-deductible HRA or limited-purpose HRA will not interfere with HSA-eligibility. A post-deductible HRA paired with an HDHP allows for HSA-eligibility so long as the HRA doesn’t provide coverage before the individual incurs claims of at least $1,500 for single or $3,000 for family coverage (in 2023). In addition, a limited-purpose HRA (available solely to reimburse dental or vision expenses) paired with an HDHP also allows for HSA-eligibility.

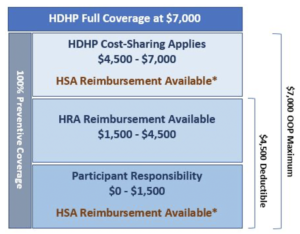

The below example illustrates an HDHP offering for single coverage with a $4,500 deductible and $7,000 maximum out-of-pocket (OOP) paired with a post-deductible HRA available to reimburse up to $3,000 in claims after $1,500 in claims have been incurred.

*HSA reimbursement available for all qualifying medical expenses for those who establish and contribute to an HSA

Finally, a combination of limited-purpose and post-deductible HRA paired with an HDHP will also allow for HSA-eligibility. For example, the HRA could provide limited-purpose reimbursement (solely for dental or vision expenses) until the minimum HDHP deductible is met ($1,500 for single; $3,000 for family in 2023) and then become available to reimburse all qualifying medical expenses once the deductible is met. This is confirmed in IRS Notice 2004-45.

In building out a plan design involving an HDHP and HRA, employers should carefully consider how it will be administered. For example, will the carrier administer the HRA, automatically applying HRA reimbursement when appropriate while administering claims? Or will there need to be coordination with a separate third-party administrator? Assuming the plan design allows for HSA-eligibility, will the employer coordinate with an HSA vendor and offer an HSA through its cafeteria plan, allowing employees to make pre-tax HSA contributions?

Once a plan design is chosen, it is important to help plan participants understand their payment responsibilities and any administrative responsibilities required to obtain HRA reimbursement, perhaps aided by illustrations similar to the one above. In addition, employees may need assistance understanding HSA eligibility, contribution and reimbursement requirements, including reimbursement coordination between the HRA and HSA.

While every effort has been taken in compiling this information to ensure that its contents are totally accurate, neither the publisher nor the author can accept liability for any inaccuracies or changed circumstances of any information herein or for the consequences of any reliance placed upon it. This publication is distributed on the understanding that the publisher is not engaged in rendering legal, accounting or other professional advice or services. Readers should always seek professional advice before entering into any commitments.